General Instructions:

1) This question paper contains two parts A and B.

2) Part A is compulsory for all.

3) Part B has two options-Financial statement Analysis and Computerised Accounting.

4) Attempt only one option of Part B.

5) All parts of a question should be attempted at one place.Section A

i. This section consists of 18 questions.

ii. All the questions are compulsory.

iii. Question Nos. 1 to 6 are very short-answer questions carrying 1 mark each.

iv. Question Nos. 7 to 10 carry 3 marks each.

v. Question Nos. 11 and 12 carry 4 marks each.

vi. Question Nos. 13 to 15 carry 6 marks each.

vii. Question Nos. 16 and 17 carry 8 marks each.Section B

i. This section consists of 6 questions.

ii. All questions are compulsory

iii. Question Nos. 18 and 19 are very short-answer questions carrying 1 mark each.

iv. Question Nos. 20 to 22 carry 3 marks.

v. Question No. 23 carries 6 marks.

Q1 :On the retirement of Hari from the firm of ‘Hari, Ram and Sharma’ the balance-sheet showed a debit balance of Rs 12,000 in the profit and loss account. For calculating the amount payable to Hari this balance will be transferred

(a) to the credit of the capital accounts of Hari, Ram and Sharma equally

(b) to the debit of the capital accounts of Hari, Ram and Sharma equally

(c) to the debit of the capital accounts of Ram and Sharma equally

(d) to the credit of the capital accounts of Ram and Sharma equally

Answer :

At the time of retirement of a partner, the balance of accumulated profits and losses is transferred among all the partners (including the retiring partner) in the old ratio. Here, debit balance of Rs 12,000 in the Profit and Loss Account will be debited (being a loss) to the capital accounts of Hari, Ram and Sharma equally.

Hence, the correct answer is option (b).

Q2 :Kumar, Verma and Naresh were partners in a firm sharing profit & loss in the ratio of 3 : 2 : 2. On 23rd January, 2015 Verma died. Verma’s share of profit till the date of his death was calculated at Rs 2,350.

Pass necessary journal entry for the same in the books of the firm.

Answer :

The Journal entry for transferring Verma”™s share of profit to his capital account is given below

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

||||

|

|

|||||

Q3 :Give the meaning of forfeiture of shares.

Answer :

Cancellation of shares on non-payment of due calls is known as forfeiture of shares.

Q4 : Joy Ltd. issued 1,00,000 equity shares of Rs 10 each. The amount was payable as follows :

On application − Rs 3 per share

On allotment − Rs 4 per share.

On 1st and final call − balance

Applications for 95,000 shares were received and shares were allotted to all the applicants. Sonam to whom 500 shares were allotted failed to pay allotment money and Gautam paid his entire amount due including the amount due on first and final call on the 750 shares allotted to him along with allotment. The amount received on allotment was

(a) Rs 3,80,000

(b) Rs 3,78,000

(c) Rs 3,80,250

(d) Rs 4,00,250

Answer :

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Hence, the correct answer is option (c).

Q5 : In the absence of partnership deed the profits of a firm are divided among the partners :

(a) In the ratio of capital

(b) Equally

(c) In the ratio of time devoted for the firm’s business

(d) According to the managerial abilities of the partners

Answer :

In the absence of partnership deed, the provisions of Indian Partnership Act, 1932 applies. According to the Partnership Act, the profits and losses are to be shared equally among the partners.

Hence, the correct answer is option (b).

Q6 : A, B, C and D were partners in a firm sharing profits in the ratio of 4 : 3 : 2 : 1. On 1-1-2015 they admitted E as a new partner for share in the profits. E brought Rs 10,000 for his share of goodwill premium which was correctly recorded in the books by the accountant. The accountant showed goodwill at Rs 1,00,000 in the books. Was the accountant correct in doing so? Give reason in support of your answer.

Answer :

Accounting Standard 26 (AS-26) prescribes that goodwill is recorded in the books only when it is purchased. Thus, at the time of admission of a partner, if the incoming partner (here E) contributes some amount towards his share of goodwill (Rs 10,000), then such goodwill should be immediately distributed among the sacrificing partners in their sacrificing ratio (since no consideration is paid by the firm for the share of goodwill brought in by E).

In this case, the accountant has shown the goodwill of the firm (Rs 1,00,000) as an asset in the books of the firm. This is certainly violating the rules contained in the AS-26, as goodwill cannot be shown in the books until it is purchased. Thus, here the accountant has adopted the wrong accounting treatment.

Q7 :Securities premium can also be utilized for three other purposes besides (i) ‘Issuing fully paid bonus shares’ and (ii) ‘Buy back of shares’. State those purposes.

Answer :

The Companies Act, 1956 imposes certain restrictions on utilisation of amount received as securities premium. As per the Section 78 of the Companies Act 1956, the amount of securities premium received can be utilised for following purposes:

i. For writing off preliminary expenses of the company.

ii. For writing off the expenses of, or the commission paid or the discount allowed on, any issue of share or debenture of the company.

iii. For paying up premium payable on redemption of redeemable preference shares or debentures of the company.

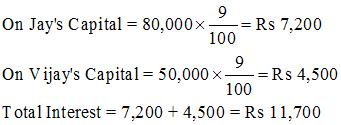

Q8 : On 1-4-2013 Jay and Vijay, entered into partnership for supplying laboratory equipments to government schools situated in remote and backward areas. They contributed capitals of Rs 80,000 and Rs 50,000 respectively and agreed to share the profits in the ratio 3 : 2. The partnership deed provided that interest on capital shall be allowed at 9% per annum. During the year the firm earned a profit of Rs 7,800.

Showing your calculations clearly, prepare ‘Profit and Loss Appropriation Account’ of Jay and Vijay for the year ended 31-3-2014.

Answer :

|

Profit and Loss Appropriation Account

|

||||

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|||

|

|

|

|

||

|

|

|

|||

Working Notes:

WN1: Calculation of Interest on Capital WN2: Calculation of Proportionate Interest on Capital

WN2: Calculation of Proportionate Interest on Capital

.jpg)

Q9 :Sun Pharma Ltd. is registered with an authorized capital of Rs 1,00,00,000 divided into 1,00,000 equity shares of Rs 100 each. The company issued 50,000 shares at a premium of Rs 40 per shares. A shareholder holding 500 shares did not pay the final call of Rs 20 per share. His shares were forfeited.

Present the ‘Share Capital’ in the Balance Sheet of the Company as per Schedule VI Part I of the Companies Act, 1956. Also prepare notes to accounts.

Answer :

|

|

||

|

|

|

|

|

|

||

|

|

||

|

|

|

|

|

|

|

|

|

|

||

|

|

||

|

|

||

|

|

|

|

|

|

||

|

|

|||

|

|

|

|

|

|

|

|

||

|

|

|||

|

|

|

||

|

|

|||

|

|

|

||

|

|

|||

|

|

|

||

|

|

|

|

|

|

|

|

||

|

|

|

||

|

|

|

||

|

|

|

||

Q10 : ‘Sangam Woollens Ltd.’, Ludhiana, are the manufactures and exporters of woollen garments. The company decided to distribute free of cost woollen garments to 10 villages of Lahaul and Spiti District of Himachal Pradesh. The company also decided to employ 50 young persons from these village in its newly established factory. The company issued 40,000 equity shares of Rs 10 each and 1,000 9% debentures of Rs 100 each to the vendors for the purchase of machinery of Rs 5,00,000.

Pass necessary Journal Entries. Also identify any one value that the company wants to communicate to the society.

Answer :

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|

||||

|

|

|||||

Values involved in the above scenario:

(i) Creation of employment opportunities

(ii) Working for social welfare

Q11 :Sunny, Honey and Rupesh were partners in a firm. On 31-3-2014 their Balance Sheet was as follows :

| Liabilities | Amount Rs |

Assets | Amount Rs |

|

| Creditors | 10,000 | Plant and machinery | 40,000 | |

| General Reserve | 30,000 | Furniture | 15,000 | |

| Capitals : | Investments | 20,000 | ||

| Sunny | 30,000 | Debtors | 20,000 | |

| Honey | 30,000 | Stock | 25,000 | |

| Rupesh | 20,000 | 80,000 | ||

| 1,20,000 | 1,20,000 | |||

Honey dies on 31-12-2014. The partnership deed provides that the representatives of the deceased partner shall be entitled to :

(i) Balance in the capital account of the deceased partner.

(ii) Interest on capital @ 6% p.a. upto the date of his death.

(iii) His share in the undistributed profits or losses as per the balance sheet.

(iv) His share in the profit of the firm till the date of his death, calculated on the basis of rate of net profit on sales of the previous year. The rate of net profit on sale of previous year was 20%. Sales of the firm during the year till 31-12-2014 was Rs 6,00,000.

Prepare Honey’s Capital Account to be presented to his executors.

Answer :

|

|

|||||

|

|

|

||||

|

|

|

|

|

||

|

|

|

|

|

||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

||||

Working Notes:

WN1 Calculation of Interest on Honey”™s Capital![]() WN2 Calculation of Honey”™s share in profits

WN2 Calculation of Honey”™s share in profits

.jpg) WN3 Calculation of Honey”™s Share in General Reserve

WN3 Calculation of Honey”™s Share in General Reserve![]()

Q12 :Kumar, Gupta and Kavita were partners in a firm sharing profits and losses equally. The firm was engaged in the storage and distribution of canned juice and its godowns were located at three different places in the city. Each godown was being managed individually by Kumar, Gupta and Kavita. Because of increase in business activities at the godown managed by Gupta, he had devote more time. Gupta demanded that his share in the profits of the firm be increased, to which Kumar and Kavita agreed. The new profit sharing ratio was agreed to be 1 : 2 : 1. For this purpose the goodwill of the firm was valued at two years purchase of the average profits of last five years. The profits of the last five years were as follows :

| Year | Profit (Rs) |

| I | 4,00,000 |

| II | 4,80,000 |

| III | 7,33,000 |

| IV (Loss) | 33,000 |

| V | 2,20,000 |

You are required to :

(i) Calculate the goodwill of the firm.

(ii) Pass necessary Journal Entry for the treatment of goodwill on change in profit sharing ratio of Kumar, Gupta and Kavita,

Answer :

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

||||

|

|

|

||||

|

|

|||||

Working Notes:

WN1 Calculation of Gaining Ratio

Old Ratio = 1 : 1 : 1

New Ratio = 1 : 2 : 1

Gaining Ratio = New Ratio – Old Ratio

![]() Only Gupta is gaining; Kumar and Kavita are sacrificing in the ratio of 1 : 1

Only Gupta is gaining; Kumar and Kavita are sacrificing in the ratio of 1 : 1

WN2 Calculation of Goodwill of the firm

.jpg) Goodwill is calculated on the basis of two years purchase of last 5 years average profit

Goodwill is calculated on the basis of two years purchase of last 5 years average profit

Goodwill = 2 × Average Profit

= 2 × 3,60,000 = 7,20,000

![]()

Q13 : Bora, Singh and Ibrahim were partners in a firm sharing profits in the ratio of 5 : 3 : 1. On 2-3-2015 their firm was dissolved. The assets were realized and the liabilities were paid off. Given below are the Realisation Account, Partners’ Capital Account and Bank Account of the firm. The accountant of the firm left a few amounts unposted in these accounts. You are required to complete these accounts by posting the correct amounts.

| Realisation Account | ||||||||

| Dr. | Cr. | |||||||

| Particulars | Amount Rs |

Particulars | Amount Rs |

|||||

| To Stock | 10,000 | By Provision of bad debts | 5,000 | |||||

| To Debtors | 25,000 | By Sundry Creditors | 16,600 | |||||

| To Plant and Machinery | 40,000 | By Bills Payable | 3,400 | |||||

| To Bank: | By Mortgage Loan | 15,000 | ||||||

| Sundry Creditors | 16,000 | By Bank-assets realized : | 30,600 | |||||

| Bills Payable | 3,400 | Stock | 6,700 | |||||

| Mortgage Loan | 15,000 | 34,400 | Debtors | 12,500 | ||||

| To Bank (Outstanding repairs) | 400 | Plant & Machinery | 36,000 | 55,200 | ||||

| To Bank (Exp.) | 620 | By Bank-unrecorded assets realized | 6,220 | |||||

| By ________ | – | |||||||

| 1,10,420 | 1,10,420 | |||||||

| Capital Accounts | ||||||||

| Dr. | Cr. | |||||||

| Particulars | Bora Rs |

Singh Rs |

Ibrahim Rs |

Particulars | Bora Rs |

Singh Rs |

Ibrahim Rs |

|

| – | – | – | – | By Balance b/d | 22,000 | 18,000 | 10,000 | |

| – | – | – | – | By General Reserve | 2,500 | 1,500 | 500 | |

| 24,500 | 19,500 | 10,500 | 24,500 | 19,500 | 10,500 | |||

| Bank Account | |||||

| Dr. | Cr. | ||||

| Particulars | Amount Rs |

Particulars | Amount Rs |

||

| To Balance b/d | 19,500 | By Relaisation (liabilities) | 34,400 | ||

| To Realisation (assets realized) | 55,200 | By Realisation (unrecorded liabilities) | 400 | ||

| ________________ | ____ | By ____________ | ____ | ||

| By ____________ | ____ | ||||

| 80,920 | 80,920 | ||||

Answer :

|

|

|||||||

|

|

|

||||||

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

|

|

|||||

|

|

|

|

|||||

|

|

|

|

|

||||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|||

|

|

|

|

|

||||

|

|

|||||||

|

|

|

||||||

|

|

|

||||||

|

|

|

|

|||||

|

|

|

||||||

|

|

|||||||

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

|

|

|

|

|

||

|

|

||||||

|

|

|

|||||

|

|

|

|

|

|||

|

|

|

|

|

|||

|

|

|

|

|

|||

|

|

|

|

|

|||

Q14 :On 1-4-2010 Sahil and Charu entered into partnership for sharing profits in the ratio of 4 : 3. They admitted Tanu as a new partner on 1-4-2012 for share which she acquired equally from Sahil and Charu. Sahil, Charu and Tanu earned profits at a higher rate than the normal rate of return for the year ended 31-3-2013. Therefore, they decided to expand their business. To meet the requirements of additional capital they admitted Puneet as a new partner on 1-4-2013 for share in profits which he acquired from Sahil and Charu in 7 : 3 ratio.

Calculate:

(i) New profit sharing ratio of Sahil, Charu and Tanu for the year 2012-13.

(ii) New profit sharing ratio of Sahil, Charu, Tanu and Puneet on Puneet’s admission.

Answer :

(i) Calculation of New Profit Sharing Ratio of Sahil, Charu and Tanu for the year 2012-13

Old Ratio of Sahil and Charu = 4 : 3

Tanu was admitted for 1/5th share, which was acquired by her equally from Sahil and Charu

Sacrificing Share

![]()

![]()

New Profit Share = Old Share – Sacrificing Share

![]()

![]()

![]()

Therefore, New Profit Sharing Ratio of Sahil, Charu and Tanu = 33 : 23 : 14

(ii) Calculation of New Profit Sharing Ratio of Sahil, Charu, Tanu and Puneet

Old Ratio of Sahil, Charu and Tanu = 33 : 23 : 14

Puneet was admitted for 1/7th share, which he acquired from Sahil and Charu in the ratio of 7 : 3

Sacrificing Share

![]()

![]()

New Profit Share = Old Share – Sacrificing Share

![]()

![]()

![]()

![]()

Therefore, New Profit Sharing Ratio of Sahil, Charu, Tanu and Puneet = 26 : 20 : 14 : 10

Q15 :Bharat Ltd. had an authorized capital of Rs 20,00,000 divided into 2,00,000 equity shares of Rs 10 each. The company issued 1,00,000 shares and the dividend paid per share was Rs 2 for the year ended 31-3-2008. The management of the company decided to export its products to the neighbouring countries Nepal, Bhutan, Sri Lanka and Bangladesh. To meet the requirement of additional funds the financial manager of the company put up the following three alternatives before its Board of Directors :

(i) Issue 54,000 equity shares.

(ii) Obtain a loan from Import and Export Bank of India. The loan was available at 12% per annum interest.

(iii) To issue 9% Debentures at a discount of 10%.

After comparing the available alternatives the company decided on 1-4-2008 to issue 6,000 9% debentures of Rs 100 each at a discount of 10%. These debentures were redeemable in four instalments starting from the end of third year. The amount of debentures to be redeemed at the end of third, fourth, fifth and sixth year was as follows :

| Year | Profit Rs |

| III | 1,00,000 |

| IV | 1,00,000 |

| V | 2,00,000 |

| VI | 2,00,000 |

Prepare 9% Debentures Account for the year 2008-09 to 2013-14.

Answer :

|

|

|||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

|

|

|

||||||||

|

|

|

|

|

|

|

||||

|

|

|

||||||||

Q16 :’Wellness Ltd.’ invited applications for issuing 40,000 equity shares of Rs 10 each at a discount of 10%. The amount was payable as follows :

On application and allotment – Rs 4 per share.

On first call – Rs 3 per share.

On second and final call – The balance.

Applications for 39,000 shares were received and allotment was made to all the applicants.

The payment was received as per the following details :

On 30,000 shares – Full amount.

On 6,000 shares – Rs 7 per share.

On 3,000 shares – Rs 4 per share.

The Directors forfeited those shares on which less than Rs 7 per share were received. The forfeited shares were re-issued at Rs 8 per share as fully paid up.

Pass necessary Journal Entries in the books of the company for the above transactions.

OR

‘Subham Ltd.’ invited applications for issuing 12,000 equity shares of Rs 10 each at a premium of Rs 3 per share. The amount was payable as follows :

On application and allotment – Rs 6 per share. (Including Premium)

On first call – Rs 4 per share.

On second and final call – The balance.

Applications for 18,000 shares were received and pro-rata allotment was made to all the applicants.

Excess money received with applications was adjusted towards sums due on first call. All calls were made and were dully received except the first call and second and final call on 120 shares allotted to Vibhu. His shares were forfeited. The forfeited shares were reissued at the maximum permissible discount as per the provisions of the Companies Act, 1956.

Pass necessary Journal Entries for the above transactions in the books of the company.

Answer :

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|||||

|

|

|

|

|||

|

|

|

||||

|

|

|

||||

Q17 : Charu and Harsha were partners in a firm sharing profits in the ratio of 3 : 2. On 1-4-2014 their Balance Sheet was as follows :

|

Balance Sheet of Charu and Harsha as on 1-4-2014 |

||||

|

Liabilities |

Amount Rs |

Assets |

Amount Rs |

|

|

Creditors |

17,000 |

Cash |

6,000 |

|

|

General Reserve |

4,000 |

Debtors |

15,000 |

|

|

Workmen Compensation Fund |

9,000 |

Investments |

20,000 |

|

|

Investment Fluctuation Fund |

11,000 |

Plant |

14,000 |

|

|

Provision for bad debts |

2,000 |

Land and Building |

38,000 |

|

|

Capitals : |

||||

|

Charu |

30,000 |

|||

|

Harsha |

20,000 |

50,000 |

||

|

93,000 |

93,000 |

|||

On the above date Vaishali was admitted for 1/4th share in the profits of the firm on the following terms :

(a) Vaishali will bring Rs 20,000 for her capital and Rs 4,000 for her share of goodwill premium.

(b) All debtors were considered good.

(c) The market value of investments was Rs 15,000.

(d) There was a liability of Rs 6,000 for workmen compensation.

(e) Capital accounts of Charu and Harsha are to be adjusted on the basis of Vaishali’s capital by opening current accounts.

Prepare Revaluation Account and Partners’ Capital Accounts.

OR

Amit, Balan and Chander were partners in a firm sharing profits in the proportion of respectively. Chander retired on 1-4-2014. The Balance Sheet of the firm on the date of Chander’s retirement was as follows :

|

Balance Sheet of Amit, Balan and Chander as on 1-4-2014 |

|||||

|

Liabilities |

Amount Rs |

Assets |

Amount Rs |

||

|

Sundry Creditors |

12,600 |

Bank |

4,100 |

||

|

Provident Fund |

3,000 |

Debtors |

30,000 |

||

|

General Reserve |

9,000 |

Less : Provision |

1,000 |

29,000 |

|

|

Capitals : |

Stock |

25,000 |

|||

|

Amit |

40,000 |

Investments |

10,000 |

||

|

Balan |

36,500 |

Patents |

5,000 |

||

|

Chander |

2,000 |

96,500 |

Machinery |

48,000 |

|

|

1,21,100 |

1,21,100 |

||||

It was agreed that :

(a) Goodwill will be valued at Rs 27,000.

(b) Depreciation of 10% was to be provided on machinery.

(c) Patents were to be reduced by 20%.

(d) Liability on account of Provident Fund was estimated at Rs 2,400.

(e) Chander took over investments for Rs 15,800.

(f) Amit and Balan decided to adjust their capitals in proportion of their profit sharing ratio by opening current accounts.

Prepare Revaluation Account and Partners’ Capital Accounts on Chander’s retirement.

Answer :

|

|

||||||

|

|

|

|||||

|

|

|

|

|

|||

|

|

|

|

||||

|

|

|

|||||

|

|

|

|

||||

|

|

|

|||||

|

|

|||||||

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|||||

|

|

|

|

|||||

|

|

|

|

|||||

|

|

|

|

|||||

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

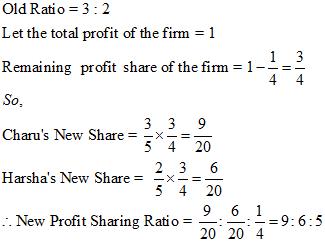

Working Notes:

WN1 Calculation of New Profit Sharing Ratio

WN2 Calculation of Sacrificing Ratio

.jpg)

WN3 Distribution of Goodwill

.jpg)

WN4 Adjustment of Capital

.jpg)

OR

|

|

|||||

|

|

|

||||

|

|

|

|

|

||

|

|

|

|

|

||

|

|

|

||||

|

|

|

||||

Q18 :Which of the following is not included in cash and cash equivalents ?

(a) Balances with banks

(b) Bank deposits with 100 days of maturity

(c) Cheques and drafts on hand and

(d) Cash on hand

Answer :

Cash and cash equivalents are short term, highly liquid investments that are readily convertible into known amount of cash and which are subject to insignificant market risk. An investment normally qualifies as cash and cash equivalents only if it has maturity period of three months. Thus, ‘Bank deposits with 100 days of maturity’ will not be included in cash and cash equivalents.

Q19 :While preparing Cash Flow statement of Sharda Ltd. ‘Depreciation provided on fixed assets’ was added to net profit to calculate cash flow from operating activities. Was the accountant correct in doing so ? Give reason.

Answer :

Depreciation on fixed assets is non-cash expense. It must have been deducted from Net Profit while preparing Profit and Loss Account. Therefore, in Cash Flow Statement it must be added back to Net Profit before taxation and extraordinary items under Cash Flow from Operating Activities. Thus, the accountant of Sharda Ltd. is correct.

Q20 :Under which heads the following items will be placed in the Balance Sheet of a company as per Schedule VI part I of the Companies Act, 1956 ?

(i) Cash in hand

(ii) Mining Rights

(iii) Short term deposits

(iv) Debenture Redemption Reserve

(v) Income received in advance

(vi) Balance of the Statement of Profit and Loss

(vii) Office Equipments and

(viii) Work-in-progress

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Q21 :From the following information related to Naveen Ltd. calculate (a) Return on Investment and (b) Total Assets to Debt Ratio.

Information : Fixed Assets Rs 75,00,000; Current Assets Rs 40,00,000; Current Liabilities Rs 27,00,000; 12% Debentures Rs 80,00,000 and Net Profit before Interest, Tax and Dividend Rs 14,50,000.

Answer :

1) Return on Investment

![]()

.jpg)

.jpg)

2) Total Assets to Debt to Ratio.jpg)

Q22 :The motto of Yash Ltd., an advertising company is ‘Service with Dignity’. Its management and work force is hard-working, honest and motivated. The net profit of the company doubled during the year ended 31-3-2014. Encouraged by its performance company decided to give one month extra salary to all its employees. Following is the Comparative Statement of Profit and Loss of the company for the years ended 31st March 2013 and 2014.

| Particulars | Note No. | 2012-13 Rs |

2013-14 Rs |

Absolute Change Rs |

% Change |

| Revenue from operations Less Employees benefit expenses Profit before tax Tax Rate 25% Profit after tax |

10,00,000 6,00,000 4,00,000 1,00,000 3,00,000 |

15,00,000 7,00,000 8,00,000 2,00,000 6,00,000 |

5,00,000 1,00,000 4,00,000 1,00,000 3,00,000 |

50 16.67 100 100 100 |

(a) Calculate Net Profit Ratio for the years ending 31st March, 2013 and 2014.

(b) Identify any two values which Yash Ltd. is trying to propagate.

Answer :

For 2013

![]()

.jpg)

For 2014

![]()

.jpg)

Q23 :Following is the Balance Sheets of Thermal Power Ltd. as at 31-3-2014 :

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

|

(a) Trade Payables |

1,79,000 | 2,04,000 | |

|

(b) Short Term Provisions

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|||

|

|

2 |

|

|

|

(ii) Intangible

|

3 | 40,000 | 1,12,000 |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Notes to Accounts :

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Answer :

|

|

||||

|

|

|

|

||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

||||

|

|

|

|||

|

|

|

|||

|

|

|

|

||

|

|

|

|||

|

|

||||

|

|

|

|||

|

|

|

|||

|

|

||||

|

|

|

|||

|

|

|

|

||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|

||

|

|

|

|||

|

|

|

|||

Working Notes:

|

|

|||

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|||