Short answers : Solutions of Questions on Page Number : 272

Q1 :What is Depreciation?

Answer : Every business acquires fixed assets for its use in the business over a period of time. As the benefits of these assets can be availed over a long period of time, thus, due to their regular use, there occurs continuous wear and tear and consequently fall in their value. This fall in the value of fixed assets, due to their regular use or expiry of time is termed as depreciation.A machinery costing Rs 1,00,000 and its useful life is 10 years; so, depreciation is calculated as:

Q2 :State briefly the need for providing depreciation.

Answer :

The needs for providing depreciation are given below.

To ascertain true net profit or net loss- Correct profit or loss can be ascertained when all the expenses and losses incurred for earning revenues are charged to Profit and Loss Account. Assets are used for earning revenues and its cost is charged in form of depreciation from Profit and Loss Account.

To show true and fair view of financial statements- If depreciation is not charged, assets are shown at higher value than their actual value in the Balance Sheet; consequently, the Balance Sheet does not reflect true and fair view of financial statements.

For ascertaining the accurate cost of production- Depreciation on plant and machinery and other assets, which are engaged in production, is included in the cost of production. If depreciation is not included, cost of production is underestimated, which will lead to low sale price and thus leads to low profit.

Distribution of dividend out of profit- If depreciation is not charged, which leads to overestimating of profit and consequently more profit is distributed as dividend, out of capital instead of the profit. This leads to the flight of scarce capital out of the business.

To provide funds for replacement of assets- Unlike other expenses, depreciation is not a cash expense. So, the amount of depreciation charged will be retained in the business and will be used for replacement of fixed assets after its useful life.

Consideration of tax- If depreciation is charged, then Profit and Loss Account will disclose lesser profit as to when the depreciation is not charged. This depicts reduced profit and thus the business will be liable for lesser tax amount.

Q3 :What are the causes of depreciation?

Answer :

Constant use – Due to constant use of the fixed assets there exists normal wear and tear that leads to fall in the value of fixed assets.

Expiry of time – With the passage of time, whether assets are used or not, its effective life decreases. The natural forces like rain, weather, etc. lead to deterioration of the fixed assets.

Obsolescence – Due to the fast technological innovations and inventions today’s assets may be outdated by tomorrow’s sophisticated assets. This leads to the obsolescence of fixed assets.

Expiry of legal rights – If an asset is acquired for a specific period of time, then, whether the asset is put to use or not, its value becomes zero at the end of its useful life. For example, if a land is acquired for Rs 1,00,000 for 25 years on lease, then each year its value depreciates by of its gross value. At the end of the 25th year, the value of the lease will be zero.

Accident – An asset may lose its value and damage may happen to it due to mishaps such as a fire accident, theft or a natural calamity. The loss due to accident is permanent in nature.

Permanent fall in value – Generally, we do not record fluctuations in the market price of the fixed assets in the books. However, if the fall in market price is permanent, it is accounted, which leads to a fall in the value of fixed assets in the books.

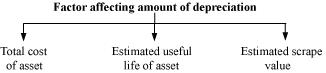

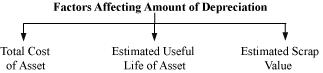

Q4 :Explain basic factors affecting the amount of depreciation.

Answer :

Total cost of asset – The total cost of an asset is taken into consideration for ascertaining the amount of depreciation. The expenses incurred in acquiring, installing and constructing asset and bringing the asset to its usable condition are included in the total cost of asset.

Estimated useful life – Every asset has its useful life other than its physical life (in terms of number of years, units, etc.), used by a business. The useful life of an asset is considered to estimate the effective life of a fixed asset. For example, land has indefinite life; however, if business acquiress a piece of land on lease for 25 years, then the useful life of the piece of land is considered to be 25 years.

Estimated scrap value – It is estimated as the net realisable value or sale value of an asset at the end of its effective life. It is deducted from the total cost of an asset. For example, furniture is acquired at Rs 50,000 and its effective life is 10 years.

After 10 years, the furniture will be sold at Rs 10,000. So, depreciation is charged as:

![]()

Q5 :Distinguish between straight line method and written down value method of calculating depreciation.

Answer :

|

Basis of Difference |

Straight Line Method |

Written Down Value Method |

|

Basis for calculation |

Depreciation is calculated on the original cost of an |

Depreciation is calculated on the reducing balance, |

|

Amount of depreciation |

Equal amount is charged each year over the effective |

Diminishing amount of depreciation (on the written down |

|

Book value of asset |

Book value of the asset becomes zero at the end of its |

Book value of the asset can never be zero. |

|

Suitability |

It is suitable for the assets like patents, copyright, |

It is suitable for assets that needs more repair in the |

|

Effect of depreciation and repair on profit and loss |

Unequal effect over the life of the asset, as |

Equal effect over the life of the asset, as |

|

Recognition under Income Tax Act |

It is not recognised under the income tax act. |

It is recognised under the income tax act. |

Q6 :In case of a long term asset, repair and maintenance expenses are expected to rise in later years than in earlier year. Which method is suitable for charging depreciation if the management does not want to increase burden on profits and loss account on account of depreciation and repair.

Answer : If the management does not want to exert undue burden on the profits due to high depreciation and repair costs in the latter years of the assets, then ‘written down method’ should be a preferred method to provide depreciation. This is because the cost of depreciation reduces; whereas, repair and maintenance expenses increase in the latter years. However, on the whole, it does not exert increasing burden on profits.

Q7 :What are the effects of depreciation on profit and loss account and balance sheet?

Answer :

The effects of depreciation on Profit and Loss Account are given below.

Depreciation increases the debit side of profit and loss account and hence reduces net profit.

Depreciation increases the total expenses, leading to an excess of debit over credit balance.

The effects of depreciation on Balance Sheet are given below.

It reduces the original cost or book value of the concerned asset.

It reduces the overall balance of asset’s column in the balance sheet.

Q8 :Distinguish between provision and reserve.

Answer :

|

Basis of Difference |

Provision |

Reserve |

|

Meaning |

It is created to meet the known liability. |

It is created to meet unknown liability. |

|

Nature |

Provision is charged against profit. |

Reserve is appropriation of the profit. |

|

Purpose |

It is created for a specific liability. |

It is created for strengthening the financial position. |

|

Mode of creation |

It is created by debiting the profit and loss account. |

It is created by debiting the profit and loss |

|

Use for payment of dividend |

It cannot be used for payment of dividends. |

It can be used for payment of dividends. |

|

Creation |

Creation of provision is compulsory. It is created even |

Creation of reserve depends on the discretion of the |

Q9 :Give four examples each of provision and reserves.

Answer :

Four examples of provision are given below.

Provision for bad and doubtful debts

Provision for discount on debtors

Provision for depreciation

Provision for taxation

Four examples of reserve are given below.

General reserve

Capital reserve

Dividend equalisation reserve

Debenture redemption reserve

Q10 :Distinguish between revenue reserve and capital reserve.

Answer :

|

Basis of Difference |

Revenue Reserve |

Capital Reserve |

|

Source |

It is created out of revenue profit, i.e., revenue |

It is created out of capital profit, i.e., gain from |

|

Dividend |

It can be used for dividend. |

It cannot be used for dividend. |

|

Purpose |

It is created for strengthening the financial position |

It is created for the purpose laid down in the |

Q11 :Give four examples each of revenue reserve and capital reserves.

Answer :

Four examples of revenue reserve are given below.

General Reserve

Retained Earnings

Dividend Equalisation Reserve

Debenture Redemption Reserve

Four examples of capital reserve are given below.

Issues of shares at premium

Profit or issue of shares

Sale of fixed assets

Profit on redemption of debentures

Q12 :Distinguish between general reserve and specific reserve.

Answer :

|

Basis of Difference |

General Reserve |

Specific Reserve |

|

Meaning |

When the reserve is created without any specified |

When reserve is created for some specific purpose, the |

|

Usage |

It can be used for any purpose. |

It cannot be used for any purpose other than the |

|

Examples |

Retained earnings, reserve funds, etc. |

Debenture redemption reserve, dividend equalisation |

Q13 :Explain the concept of secret reserve.

Answer :

Reserves that are created by overstating liabilities or understating assets are known as secret reserves. They are not shown in the balance sheet. These reduce tax liabilities, as the liabilities are overstated. It is created by management to avoid competition by reducing profit. Creation of secret reserve is not allowed by Companies Act, 1956 that requires full disclosure of all material facts and accounting policies while preparing final statements.

Long answers : Solutions of Questions on Page Number : 273

Q1 :Explain the concept of depreciation. What is the need for charging depreciation and what are the causes of depreciation?

Answer :

Every business acquires fixed assets for its use in the business over a period of time. As the benefits of these assets can be availed over a long period of time (due to their regular use), there exists continuous wear and tear and consequently fall in their value. This fall in the value of fixed assets (due to regular use or expiry of time) is termed as depreciation.

A machinery that costs Rs 1,00,000 and its useful life of 10 years, its depreciation will be calculated as:

To ascertain true net profit or net loss – Correct profit or loss can be ascertained when all the expenses and losses incurred for earning revenues are charged to profit and loss account. Assets are used for earning revenues and its cost is charged in form of depreciation from profit and loss account.

To show true and fair view of financial statements – If depreciation is not charged, assets are shown at higher value than their actual value in the balance sheet; consequently, the balance sheet does not reflect true and fair view of financial statements.

For ascertaining the accurate cost of production – Depreciation on plant and machinery and other assets, which are engaged in production, is included in the cost of production. If depreciation is not included, cost of production is underestimated, which will lead to low sale price and thus leads to low profit.

Distribution of dividend out of profit – If depreciation is not charged, which leads to overestimating of profit and consequently more profit is distributed as dividend, out of capital instead of the profit. This leads to the flight of scarce capital out of the business.

To provide funds for replacement of assets – Unlike other expenses, depreciation is not a cash expense. So, the amount of depreciation charged will be retained in the business and will be used for replacement of fixed assets after its useful life.

Consideration of tax – If depreciation is charged, then profit and loss account will disclose lesser profit as to when the depreciation is not charged. This depicts reduced profit and thus the business will be liable for lesser tax amount.

Below are given the causes for depreciation.

Constant use – Due to constant use of the fixed assets there exists normal wear and tear that leads to fall in the value of fixed assets.

Expiry of time – With the passage of time, whether assets are used or not, its effective life decreases. The natural forces like rain, weather, etc. lead to deterioration of the fixed assets.

Obsolescence – Due to the fast technological innovations and inventions today’s assets may be outdated by tomorrow’s sophisticated assets. This leads to the obsolescence of fixed assets.

Expiry of legal rights – If an asset is acquired for a specific period of time, then, whether the asset is put to use or not, its value becomes zero at the end of its useful life. For example, if a land is acquired for Rs 1,00,000 for 25 years on lease,

then each year its value depreciates by ![]() of its gross value. At the end of the 25th year, the value of the lease will be zero.

of its gross value. At the end of the 25th year, the value of the lease will be zero.

Accident – An asset may lose its value and damage may happen to it due to mishaps such as a fire accident, theft or a natural calamity. The loss due to accident is permanent in nature.

Permanent fall in value – Generally, we do not record fluctuations in the market price of the fixed assets in the books. However, if the fall in market price is permanent, it is accounted, which leads to a fall in the value of fixed assets in the books.

Q2 :Discuss in detail the straight line method and written down value method of depreciation. Distinguish between the two and also give situations where they are useful.

Answer :

Straight Line method

It is a simple method of charging depreciation. Under this method, depreciation is charged on the original cost of an asset, at a fixed rate of percentage. In this method, amount of depreciation remains same from year to year and asset’s value becomes zero at the end of its useful life.

Amount of depreciation is calculated as under:

![]()

Advantages of Straight Line Method

It is simple to calculate.

Asset can be completely written off, i.e., asset can be depreciated until the net scrap value is zero.

Same amount of depreciation is charged every year. Therefore, it helps in easy comparison of Profit and Loss Account for different years.

It is used for assets that have low repairs and maintenance expenses and are continuously used over a period of time.

Limitations of Straight Line Method

Burden of deprecation is more on profit and loss account in the later years, when repair and maintenance costs increase, as asset becomes older.

Value of asset becomes zero in the books even if asset is still in usable condition in business.

Uses of Straight Line Method

This method is useful where repairs and maintenance expenses on asset are low.

It is also useful when an asset is continuously used from one year to another.

It is useful when the value of assets, such as patent, copyright, goodwill, etc., becomes zero

Written Down Value Method

This method is applicable where depreciation is charged on the diminishing balance, i.e., book value of the asset. In this method, asset’s value goes on diminishing year after year and the amount of depreciation declines.

Rate of depreciation is calculated as follows:

Where,

R represents rate of depreciation

n represents expected useful life of the asset

s represents the scrap value

c represents the cost of the asset

Advantages of Written Down Value Method

It is based on the logical assumption that asset is used more in the earlier years, so more cost is charged in form of depreciation.

It is suitable for the assets where repairs are more in the later years, as depreciation is lesser and on a whole the combined burden of depreciation and repairs exerts equal pressure on the net profit over years.

This method is accepted by the income tax authorities.

As more depreciation is charged in the earlier years, so the loss due to obsolescence of the asset is reduced.

Limitations of Written Down Value Method

It is difficult to calculate and is a time consuming process.

The value of an asset cannot be zero, thus the asset cannot be completely written off.

There arises shortage of funds for replacement of new asset. This happens due to the fact that the amount of depreciation is retained and used in the business. Consequently, at the end of the useful life of an old asset, business finds it difficult to arrange funds for its replacement.

Uses of Written Down Value Method

It is useful when assets have long life.

It is useful for those assets that require more repair and maintenance costs in the later years.

It provides easy calculation to provide depreciation of additional asset purchased during a year.

Difference between Straight Line Method and Written Down Value Method

|

Basis of Difference |

Straight Line Method |

Written Down Method |

|

Basis for calculation |

Depreciation is calculated on the original cost of an |

Depreciation is calculated on the reducing balance, |

|

Amount of depreciation |

Equal amount is charged each year over the effective |

Diminishing amount of depreciation (on the written down |

|

Book value of asset |

Book value of the asset becomes zero at the end of its |

Book value of the asset can never be zero. |

|

Suitability |

It is suitable for the assets like, patents, |

It is suitable for assets that needs more repairs and |

|

Effect of depreciation and repair on profit and loss |

Unequal effect over the life of the asset, as |

Equal effect over the life of the asset, as |

|

Recognition under Income Tax Act |

It is not recognised under the Income Tax Act. |

It is recognised under the Income Tax Act. |

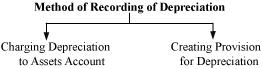

Q3 :Describe in detail two methods of recording depreciation. Also give the necessary journal entries.

Answer :

The two methods of recording depreciation are diagrammatically presented below.

Charging depreciation to Asset Account- Under this method, depreciation is directly credited to the asset account and no separate account is prepared for provision of depreciation. Under this method, the original cost of an asset and the total amount of depreciation cannot be determined from the Balance Sheet, as the Asset Account appears at its written down value.

Journal entries for depreciation are given below.

When depreciation is charged to Assets Account

| Depreciation A/c |

Dr. |

|

| To Assets A/c | ||

| (Depreciation charged to Assets Account) | ||

Closing of Depreciation Account

| Profit and Loss A/c | Dr. | |

| To Depreciation A/c | ||

| (Depreciation transferred to Profit and Loss Account) | ||

Creating Provision for Depreciation Account- Under this method, depreciation is not credited to the Assets Account; in fact, it is credited to the provision for Depreciation Account. At the year end, asset is shown at the original cost in the Balance Sheet and total depreciation up to the date of Balance Sheet is shown as Provision for Depreciation Account.

Journal entries for depreciation are:

Charging Depreciation

| Depreciation A/c |

Dr. |

|

| To Provision for Depreciation A/c | ||

| (Depreciation charged) | ||

Closing of Depreciation Account

| Profit and Loss A/c |

Dr. |

|

| To Depreciation A/c | ||

| (Depreciation account is transferred to Profit and Loss Account) |

||

When the asset is sold, the accumulated depreciation on that asset is credited to the Asset Account by passing the following Journal entry:

| Provision for Depreciation A/c |

Dr. |

|

| To Asset A/c | ||

| (Accumulated depreciation transferred to Assets Account) | ||

Q4 :Explain determinants of the amount of depreciation.

Answer :

Total cost of asset – The total cost of an asset is taken into consideration for ascertaining the amount of depreciation. The expenses incurred in acquiring, installing and constructing of assets and bringing the assets to their usable condition are included in the total cost of asset.

Estimated useful life – Every asset having it’s useful life other than it’s physical life, in terms of number of years, units, etc. are considered to estimate the effective life of a fixed asset. For example, land has indefinite life; however, if business acquires a piece of land on lease for 25 years, it’s useful life is considered to be 25 years.

Estimated scrap value – It is estimated as the net realisable value or sale value of an asset at the end of it’s effective life. It is deducted from the total cost of an asset. For example, furniture is acquired at Rs 50,000 with it’s effective life of 10 years.

After 10 years, furniture will be sold at Rs 10,000. So, depreciation is charged as:

![]()

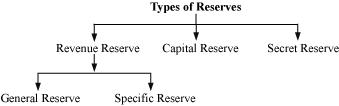

Q5 :Name and explain different types of reserves in details.

Answer :

Reserves- Reserves are created for strengthening the financial positions and future growth. It is created out of profit earned by business.

The broad classification of reserve is diagrammatically presented below.

Revenue Reserve- It is created out of revenue profit, i.e., revenue earned from normal activities of the business. It can be used for either general purpose or specific purpose. It is of two types:

a. General Reserve- When the reserve is created without any specified purpose, then the reserve is called general reserve. It is a free reserve and so can be used for any purpose. It can also be used for future growth and expansion. For example, reserve funds, retained earnings, contingencies reserves, etc.

b. Specific Reserve- When reserve is created for some specific purpose, then the reserve is called specific reserve.

Examples of specific reserve are given below.

i. Debenture Redemption Reserve

ii. Investment Fluctuation Reserve

iii. Dividend Equalisation Reserve

iv. Workmen Compensation Fund

Capital Reserve- It is created out of capital profit, i.e., gain from other than normal activities of business operations, such as sale of fixed asset, etc. It is created to meet the capital loss. It cannot be distributed as dividend. The example of capital reserves are given below.

i. Premium on issue of shares

ii. Premium on issue of debentures

iii. Profit on redemption of debentures

iv. Profit on sale of fixed assets

v. Profit on reissue of forfeited shares

vi. Profit prior to incorporation

Secret Reserves- Reserves that are created by overstating liabilities or understating assets are known as secret reserves. They are not shown in the Balance Sheet. These reduce tax liabilities, as the liabilities are overstated. It is created by management to avoid competition by reducing profit. Creation of secret reserve is not allowed by Companies Act, 1956, which requires full disclosure of all materials facts and accounting policies, while preparing final statements.

Q6 :What are provisions? How are they created? Give accounting treatment in case of provision for doubtful Debts.

Answer :

Provisions are the amount that is created against profit to meet the known liability; however, the amount of liability is uncertain. It is created for specific liability. Creation of provision is compulsory even if, there is no profit. The underlying principle behind creation of provision is conservatism, viz., to prepare for future loss. The main rationale for making provisions is to provide cushion to the future business performance against the uncertain and unforeseen losses that may arise from the past transactions. A few examples of provisions are given below.

Provision for bad and doubtful debts

Provision for depreciation

Provision for taxation

Provision for discount on debtors

Provisions are made by debiting the Profit and Loss Account on estimate basis. The provisions are created on the basis of past experiences. Every year, a business may experience common losses, such as depreciation of fixed assets, taxation, etc., which are although known; however, their exact amount of future period is unknown. Thus, business creates provision of certain percentage every year, which is truly based on the intuitions and past experiences. These unascertained liabilities in form of provisions are kept aside, which help future business activities, undisturbed from the future losses.

Accounting treatment for provision for doubtful debts is:

| Profit and Loss A/c |

Dr. |

|

| To Provision for Doubtful Debts | ||

| (Provision for doubtful debt made) | ||

Numerical questions : Solutions of Questions on Page Number : 273

Q1 : On April 01, 2000, Bajrang Marbles purchased a Machine for Rs 2,80,000 and spent Rs 10,000 on its carriage and Rs 10,000 on its installation. It is estimated that its working life is 10 years and after 10 years its scrap value will be Rs 20,000.

(a) Prepare Machine account and Depreciation account for the first four years by providing depreciation on straight line method. Accounts are closed on March 31st every year.

(b) Prepare Machine account, Depreciation account and Provision for depreciation account (or accumulated depreciation account) for the first four years by providing depreciation using straight line method accounts are closed on March 31 every year.

Answer :

|

Books of Bajrang Marbles |

||||||||

|

(a) |

||||||||

|

Machinery Account |

||||||||

|

Dr. |

Cr. |

|||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

|

2000 |

2001 |

|||||||

|

Apr.01 |

Bank |

3,00,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

Balance c/d |

2,72,000 |

|||||||

|

3,00,000 |

3,00,000 |

|||||||

|

2001 |

2002 |

|||||||

|

Apr.01 |

Balance b/d |

2,72,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

Mar.31 |

Balance c/d |

2,44,000 |

||||||

|

2,72,000 |

2,72,000 |

|||||||

|

2002 |

2003 |

|||||||

|

Apr.01 |

Balance b/d |

2,44,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

Mar.31 |

Balance c/d |

2,16,000 |

||||||

|

2,44,000 |

2,44,000 |

|||||||

|

2003 |

2004 |

|||||||

|

Apr.01 |

Balance b/d |

2,16,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

Mar.31 |

Balance c/d |

1,88,000 |

||||||

|

2,16,000 |

2,16,000 |

|||||||

Note: As per solution, the closing balance of machinery account at the end of fourth year is Rs 1,88,000; whereas, the answer given in the book is Rs 1,28,000

However, if we would have taken purchase price of machine Rs 1,80,000 instead of Rs 2,80,000 then the closing balance would have been be Rs 1,28,000

Working notes: Calculation of annual depreciation

(b)

Provision for Depreciation Account

|

Depreciation (p.a.) |

= |

(Original cost – Scrap Value ) |

||||||

|

Estimated Life of Asset (years) |

||||||||

|

= |

(2,80,000 + 10,000 + 10,000 – 20,000) |

|||||||

|

10 |

||||||||

|

= |

Rs 28,000 per annum |

|||||||

|

Depreciation Account |

||||||||

|

Dr. |

Cr. |

|||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

|

2001 |

2001 |

|||||||

|

Mar.31 |

Machinery |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2002 |

2002 |

|||||||

|

Mar.31 |

Machinery |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2003 |

2003 |

|||||||

|

Mar.31 |

Machinery |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2004 |

2004 |

|||||||

|

Mar.31 |

Machinery |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

Machinery Account |

||||||||

|

Dr. |

Cr. |

|||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

|

2000 |

2001 |

|||||||

|

Apr.01 |

Bank |

3,00,000 |

Mar.31 |

Balance c/d |

3,00,000 |

|||

|

3,00,000 |

3,00,000 |

|||||||

|

2001 |

2002 |

|||||||

|

Apr.01 |

Balance b/d |

3,00,000 |

Mar.31 |

Balance c/d |

3,00,000 |

|||

|

3,00,000 |

3,00,000 |

|||||||

|

2002 |

2003 |

|||||||

|

Apr.01 |

Balance b/d |

3,00,000 |

Mar.31 |

Balance c/d |

3,00,000 |

|||

|

3,00,000 |

3,00,000 |

|||||||

|

2003 |

2004 |

|||||||

|

Apr.01 |

Balance b/d |

3,00,000 |

Mar.31 |

Balance c/d |

3,00,000 |

|||

|

3,00,000 |

3,00,000 |

|||||||

|

Provision for Depreciation Account |

||||||||

|

Dr. |

Cr. |

|||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

|

2001 |

2001 |

|||||||

|

Mar.31 |

Balance c/d |

28,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2001 |

||||||||

|

Apr.01 |

Balance b/d |

28,000 |

||||||

|

2002 |

2002 |

|||||||

|

Mar.31 |

Balance c/d |

56,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

56,000 |

56,000 |

|||||||

|

2002 |

||||||||

|

Apr.01 |

Balance b/d |

56,000 |

||||||

|

2003 |

2003 |

|||||||

|

Mar.31 |

Balance c/d |

84,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

84,000 |

84,000 |

|||||||

|

2003 |

||||||||

|

Apr.01 |

Balance b/d |

84,000 |

||||||

|

2004 |

2004 |

|||||||

|

Mar.31 |

Balance c/d |

1,12,000 |

Mar.31 |

Depreciation |

28,000 |

|||

|

1,12,000 |

1,12,000 |

|||||||

|

Depreciation Account |

||||||||

|

Dr. |

Cr. |

|||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

|

2001 |

2001 |

|||||||

|

Mar.31 |

Provision for Depreciation |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2002 |

2002 |

|||||||

|

Mar.31 |

Provision for Depreciation |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2003 |

2003 |

|||||||

|

Mar.31 |

Provision for Depreciation |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

|

2004 |

2004 |

|||||||

|

Mar.31 |

Provision for Depreciation |

28,000 |

Mar.31 |

Profit and Loss |

28,000 |

|||

|

28,000 |

28,000 |

|||||||

Note: As per solution, the closing balance of Provision for Depreciation Account at the end of fourth year is Rs 1,12,000; whereas, the answer given in the book is Rs 72,000

However, if we would have taken purchase price of machine Rs 1,80,000 instead of Rs 2,80,000 then the closing balance would have been be Rs 72,000

Q2 :On July 01, 2000, Ashok Ltd. Purchased a Machine for Rs 1,08,000 and spent Rs 12,000 on its installation. At the time of purchase it was estimated that the effective commercial life of the machine will be 12 years and after 12 years its salvage value will be Rs 12,000.

Prepare machine account and depreciation Account in the books of Ashok Ltd. For first three years, if depreciation is written off according to straight line method. The account are closed on December 31st, every year.

Answer:

|

Books of Ashok Ltd. |

|||||||

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2000 |

2000 |

||||||

|

Jul.01 |

Bank |

1,20,000 |

Dec.31 |

Depreciation |

4,500 |

||

|

Dec.31 |

Balance c/d |

1,15,500 |

|||||

|

1,20,000 |

1,20,000 |

||||||

|

2001 |

2001 |

||||||

|

Jan.01 |

Balance b/d |

1,15,500 |

Dec.31 |

Depreciation |

9,000 |

||

|

Dec.31 |

Balance c/d |

1,06,500 |

|||||

|

1,15,000 |

1,15,500 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d |

1,06,500 |

Dec.31 |

Depreciation |

9,000 |

||

|

Dec.31 |

Balance c/d |

97,500 |

|||||

|

1,06,500 |

1,06,500 |

||||||

|

2003 |

|||||||

|

Jan.01 |

Balance b/d |

97,500 |

|||||

|

Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2000 |

2000 |

||||||

|

Dec.31 |

Machinery |

4,500 |

Dec.31 |

Profit and Loss |

4,500 |

||

|

4,500 |

4,500 |

||||||

|

2001 |

2001 |

||||||

|

Dec.31 |

Machinery |

9,000 |

Dec.31 |

Profit and Loss |

9,000 |

||

|

9,000 |

9,000 |

||||||

|

2002 |

2002 |

||||||

|

Dec.31 |

Machinery |

9,000 |

Dec.31 |

Profit and Loss |

9,000 |

||

|

9,000 |

9,000 |

||||||

Working Note:

|

Depreciation (p.a.) |

= |

(1,08,000 + 12,000 x 12,000) |

|

12 years |

||

|

= |

Rs 9,000 per annum |

Q3 :Reliance Ltd. Purchased a second hand machine for Rs 56,000 on October 01, 2001 and spent Rs 28,000 on its overhaul and installation before putting it to operation. It is expected that the machine can be sold for Rs 6,000 at the end of its useful life of 15 years. Moreover an estimated cost of Rs 1,000 is expected to be incurred to recover the salvage value of Rs 6,000. Prepare machine account and Provision for depreciation account for the first three years charging depreciation by fixed instalment Method. Accounts are closed on December 31, every year.

Answer :

|

Books of Reliance Ltd. |

|||||||

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2010 |

2010 |

||||||

|

Oct.01 |

Bank |

84,000 |

|||||

|

Dec.31 |

Balance c/d |

84,000 |

|||||

|

84,000 |

84,000 |

||||||

|

2011 |

2011 |

||||||

|

Jan.01 |

Balance b/d |

84,000 |

|||||

|

Dec.31 |

Balance c/d |

84,000 |

|||||

|

84,000 |

84,000 |

||||||

|

2012 |

2012 |

||||||

|

Jan.01 |

Balance b/d |

84,000 |

|||||

|

Dec.31 |

Balance c/d |

84,000 |

|||||

|

84,000 |

84,000 |

||||||

|

Provision for Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2010 |

|||||||

|

Dec.31 |

Depreciation |

1,316 |

|||||

|

2010 |

|||||||

|

Dec.31 |

Balance c/d |

1,316 |

|||||

|

1,316 |

1,316 |

||||||

|

2011 |

|||||||

|

Jan.01 |

Balance b/d |

1,316 |

|||||

|

2011 |

Dec.31 |

Depreciation |

5,267 |

||||

|

Dec.31 |

Balance c/d |

6,583 |

|||||

|

6,583 |

6,583 |

||||||

|

2012 |

|||||||

|

Jan.01 |

Balance b/d |

6,583 |

|||||

|

2012 |

Dec.31 |

Depreciation |

5,267 |

||||

|

Dec.31 |

Balance c/d |

11,850 |

|||||

|

11,850 |

11,850 |

||||||

|

2013 |

|||||||

|

Jan.01 |

Balance b/d |

11,850 |

|||||

Working Note:

|

Depreciation (p.a.) |

= |

(56,000 + 28,000 – 6,000 + 1,000) |

|

15 years |

||

|

= |

Rs 5,267 per annum |

Note: As per the solution, the balance of provision for depreciation account, as on Jan.01, 2013 is Rs 11,850; whereas, as per the book, it is Rs 18,200.

However, if we ignore the scrap value and prepare provision for depreciation for 4 years, the answer would match to that of the book.

Q4 :Berlia Ltd. Purchased a second hand machine for Rs 56,000 on July 01, 2001 and spent Rs 24,000 on its repair and installation and Rs 5,000 for its carriage. On September 01, 2002, it purchased another machine for Rs 2,50,000 and spent Rs 10,000 on its installation.

(a) Depreciation is provided on machinery @10% p.a on original cost method annually on December 31. Prepare machinery account and depreciation account from the year 2001 to 2004.

(b) Prepare machinery account and depreciation account from the year 2001 to 2004, if depreciation is provided on machinery @10% p.a. on written down value method annually on December 31.

Note*: There is a misprint in the question. The year 2001 has been misprinted as 2010. Accordingly, we have worked out the solution for the years 2001 to 2004.

Answer :

|

Books of Berlia Ltd. (a) |

|||||||

|

Machinery Account (Original Cost Method) |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Jul.01 |

Bank (i) |

85,000 |

Dec.31 |

Depreciation |

4,250 |

||

|

(5,600 + 24,000 + 5,000) |

Dec.31 |

Balance c/d |

80,750 |

||||

|

85,000 |

85,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d (i) |

80,750 |

Dec.31 |

Depreciation |

|||

|

Sep.01 |

Bank (ii) |

2,60,000 |

(i) 8,500, (ii) 8,667 |

17,167 |

|||

|

(2,50,000 + 10,000) |

Dec.31 |

Balance c/d |

3,23,583 |

||||

|

(i) 72,250, (ii) 2,51,333 |

|||||||

|

3,40,750 |

3,40,750 |

||||||

|

2003 |

2003 |

||||||

|

Jan.01 |

Balance b/d |

3,23,583 |

Dec.31 |

Depreciation |

|||

|

(i) 72,250, (ii) 2,51,333 |

(i) 8,500, (ii) 26,000 |

34,500 |

|||||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 63,750, (ii) 2,25,333 |

2,89,083 |

||||||

|

3,23,583 |

3,23,583 |

||||||

|

2004 |

Balance b/d |

2004 |

|||||

|

Jan.01 |

(i) 63,750, (ii) 2,25,333 |

2,89,083 |

Dec.31 |

Depreciation |

|||

|

(i) 8,500, (ii) 26,000 |

34,500 |

||||||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 55,250, (ii) 1,99,333 |

2,54,583 |

||||||

|

2,89,083 |

2,89,083 |

||||||

|

Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Dec.31 |

Machinery |

4,250 |

Dec.31 |

Profit and Loss |

4,250 |

||

|

4,250 |

4,250 |

||||||

|

2002 |

2002 |

||||||

|

Dec.31 |

Machinery |

Dec.31 |

Profit and Loss |

17,167 |

|||

|

(i) 8,500 (ii) 8,667 |

17,167 |

||||||

|

17,167 |

17,167 |

||||||

|

2003 |

2003 |

||||||

|

Dec.31 |

Machinery |

Dec.31 |

Profit and Loss |

34,500 |

|||

|

(i) 8,500 (ii) 26,000 |

34,500 |

||||||

|

34,500 |

34,500 |

||||||

|

2004 |

2004 |

||||||

|

Dec.31 |

Machinery |

34,500 |

Dec.31 |

Profit and Loss |

34,500 |

||

|

(i) 8,500 (ii) 26,000 |

34,500 |

34,500 |

|||||

Working notes: Calculation of annual depreciation

(i) Depreciation (p.a.) on Machinery Purchased on July 01, 2001

= (56,000 + 24,000 + 5,000) × 10⁄100

(ii) Depreciation (p.a.) on Machinery purchased on September 01, 2002.

= (2,50,000 + 10,000) × 10⁄100

|

Machinery Account (Written Down Value method) |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Jul.01 |

Bank (i) |

85,000 |

Dec.31 |

Depreciation |

4,250 |

||

|

(5,600 + 24,000 + 5,000) |

Dec.31 |

Balance c/d |

80,750 |

||||

|

85,000 |

85,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d (i) |

80,750 |

Dec.31 |

Depreciation |

|||

|

Sep.01 |

Bank (ii) |

2,60,000 |

(i) 8,075, (ii) 8,667 |

16,742 |

|||

|

(2,50,000 + 10,000) |

Dec.31 |

Balance c/d |

|||||

|

(i) 72,675, (ii) 2,51,333 |

3,24,008 |

||||||

|

3,40,750 |

3,40,750 |

||||||

|

2003 |

2003 |

||||||

|

Jan.01 |

Balance b/d |

3,24,008 |

Dec.31 |

Depreciation |

|||

|

(i) 72,675, (ii) 2,51,333 |

(i) 7,268, (ii) 25,133 |

32,401 |

|||||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 65,407, (ii) 2,26,200 |

2,91,607 |

||||||

|

3,24,008 |

3,24,008 |

||||||

|

2004 |

Balance b/d |

2004 |

|||||

|

Jan.01 |

(i) 65,407, (ii) 2,26,200 |

2,91,607 |

Dec.31 |

Depreciation |

|||

|

(i) 6,540, (ii) 22,620 |

29,160 |

||||||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 58,867, (ii) 2,03,580 |

2,62,447 |

||||||

|

2,91,607 |

2,91,607 |

||||||

|

Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Dec.31 |

Machinery |

4,250 |

Dec.31 |

Profit and Loss |

4,250 |

||

|

4,250 |

4,250 |

||||||

|

2002 |

2002 |

||||||

|

Dec.31 |

Machinery |

Dec.31 |

Profit and Loss |

16,742 |

|||

|

(i) 8,075, (ii) 8,667 |

16,742 |

||||||

|

16,742 |

16,742 |

||||||

|

2003 |

2003 |

||||||

|

Dec.31 |

Machinery |

Dec.31 |

Profit and Loss |

32,401 |

|||

|

(i) 7,268, (ii) 25,133 |

32,401 |

||||||

|

32,401 |

32,401 |

||||||

|

2004 |

2004 |

||||||

|

Dec.31 |

Machinery |

Dec.31 |

Profit and Loss |

29,160 |

|||

|

(i) 6,540, (ii) 22,620 |

29,160 |

||||||

|

29,160 |

29,160 |

||||||

Q5 :Ganga Ltd. purchased a machinery on January 01, 2001 for Rs 5,50,000 and spent Rs 50,000 on its installation. On September 01, 2001 it purchased another machine for Rs 3,70,000. On May 01, 2002 it purchased another machine for Rs 8,40,000 (including installation expenses).

Depreciation was provided on machinery @10% p.a. on original cost method annually on December 31. Prepare:

(a) Machinery account and depreciation account for the years 2001, 2002, 2003 and 2004.

(b) If depreciation is accumulated in provision for Depreciation account then prepare machine account and provision for depreciation account for the years 2001, 2002, 2003 and 2004.

Note*: There is a misprint in the question. The year 2001 has been misprinted has 2010. Accordingly, we have worked out the solution for the years 2001 to 2004.

Answer :

|

Books of Ganga Ltd. |

|||||||

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Jan.01 |

Bank (i) |

6,00,000 |

Dec.31 |

Depreciation (i) 60,000 (ii) 12,333 |

72,333 |

||

|

(5,50,000 + 50,000) |

Dec.31 |

Balance c/d |

|||||

|

Sep.01 |

Bank (ii) |

3,70,000 |

(i) 5,40,000, (ii) 3,57,667 |

8,97,667 |

|||

|

9,70,000 |

9,70,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d |

Dec.31 |

Depreciation |

||||

|

(i) 5,40,000, (ii) 3,57,667 |

8,97,667 |

(i) 60,000, (ii) 37,000, |

|||||

|

May.01 |

Bank (iii) |

8,40,000 |

(iii) 56,000 |

1,53,000 |

|||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 4,80,000 (ii) 3,20,667, |

|||||||

|

(iii) 7,84,000 |

15,84,667 |

||||||

|

17,37,667 |

17,37,667 |

||||||

|

2003 |

2003 |

||||||

|

Jan.01 |

Balance b/d |

Dec.31 |

Depreciation |

||||

|

(i) 4,80,000, (ii) 3,20,667 |

(i) 60,000, (ii) 37,000, |

||||||

|

(iii) 7,84,000 |

15,84,667 |

Dec.31 |

(iii) 84,000 |

1,81,000 |

|||

|

Balance c/d |

|||||||

|

(i) 4,20,000, (ii) 2,83,667, |

|||||||

|

(iii) 7,00,000 |

14,03,667 |

||||||

|

15,84,667 |

15,84,667 |

||||||

|

2004 |

2004 |

||||||

|

Jan.01 |

Balance b/d |

Dec.31 |

Depreciation |

||||

|

(i) 4,20,000, (ii) 2,83,667, |

(i) 60,000, (ii) 37,000, |

||||||

|

(iii) 7,00,000 |

14,03,667 |

(iii) 84,000 |

1,81,000 |

||||

|

Dec.31 |

Balance c/d |

||||||

|

(i) 3,60,000, (ii) 2,46,667, |

|||||||

|

(iii) 6,16,000 |

12,22,667 |

||||||

|

14,03,667 |

14,03,667 |

||||||

|

Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Dec.31 |

Machinery |

72,333 |

Dec.31 |

Profit and Loss |

72,333 |

||

|

72,333 |

72,333 |

||||||

|

2002 |

2002 |

||||||

|

Dec.31 |

Machinery |

1,53,000 |

Dec.31 |

Profit and Loss |

1,53,000 |

||

|

1,53,000 |

1,53,000 |

||||||

|

2003 |

2003 |

||||||

|

Dec.31 |

Machinery |

1,81,000 |

Dec.31 |

Profit and Loss |

1,81,000 |

||

|

1,81,000 |

1,81,000 |

||||||

|

2004 |

2004 |

||||||

|

Dec.31 |

Machinery |

1,81,000 |

Dec.31 |

Profit and Loss |

1,81,000 |

||

|

1,81,000 |

1,81,000 |

||||||

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Jan.01 |

Bank (i) |

6,00,000 |

|||||

|

(5,50,000 + 50,000) |

Dec.31 |

Balance c/d |

|||||

|

Sep.01 |

Bank (ii) |

3,70,000 |

9,70,000 |

||||

|

9,70,000 |

9,70,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d |

||||||

|

(i) 6,00,000 (ii) 3,70,000 |

9,70,000 |

||||||

|

May.01 |

Bank (iii) |

8,40,000 |

Dec.31 |

Balance c/d |

18,10,000 |

||

|

18,10,000 |

18,10,000 |

||||||

|

2003 |

2003 |

||||||

|

Jan.01 |

Balance b/d |

Dec.31 |

Balance c/d |

18,10,000 |

|||

|

(i) 6,00,000 (ii) 3,70,000 |

|||||||

|

(iii) 8,40,000 |

18,10,000 |

||||||

|

18,10,000 |

18,10,000 |

||||||

|

2004 |

2004 |

||||||

|

Jan.01 |

Balance b/d |

Dec.31 |

Balance c/d |

18,10,000 |

|||

|

(i) 6,00,000 (ii) 3,70,000 |

|||||||

|

(iii) 8,40,000 |

18,10,000 |

||||||

|

18,10,000 |

18,10,000 |

||||||

|

Provision for Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Dec.31 |

Balance c/d |

72,333 |

Dec.31 |

Depreciation |

72,333 |

||

|

72,333 |

72,333 |

||||||

|

2002 |

|||||||

|

2002 |

Jan.01 |

Balance b/d |

72,333 |

||||

|

Dec.31 |

Balance c/d |

2,25,333 |

Dec.31 |

Depreciation |

1,53,000 |

||

|

2,25,333 |

2,25,333 |

||||||

|

2003 |

|||||||

|

2003 |

Jan.01 |

Balance b/d |

2,25,333 |

||||

|

Dec.31 |

Balance c/d |

4,06,333 |

Dec.31 |

Depreciation |

1,81,000 |

||

|

4,06,333 |

4,06,333 |

||||||

|

2004 |

|||||||

|

2004 |

Jan.01 |

Balance b/d |

4,06,333 |

||||

|

Dec.31 |

Balance c/d |

5,87,333 |

Dec.31 |

Depreciation |

1,81,000 |

||

|

5,87,333 |

5,87,333 |

||||||

Q6 :Azad Ltd. purchased furniture on October 01, 2002 for Rs 4,50,000. On March 01, 2003 it purchased another furniture for Rs 3,00,000. On July 01, 2004 it sold off the first furniture purchased in 2002 for Rs 2,25,000. Depreciation is provided at 15% p.a. on written down value method each year. Accounts are closed each year on March 31. Prepare furniture account, and accumulated depreciation account for the years ended on March 31, 2003, March 31, 2004 and March 31,2005. Also give the above two accounts if furniture disposal account is opened.

Note*: There is a misprint in the question. The books of accounts are to be prepared for the years ending March 31, 2003, March 31, 2004 and March 31, 2005. The date March 31, 2005 has been misprinted as March 31, 2010. Accordingly, we have worked out the solution for the years 2002-03, 2003-04 and 2004-05.

Answer :

|

Books of Azad Ltd. |

|||||||

|

Furniture Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2002 |

2003 |

||||||

|

Oct.01 |

Bank (i) |

4,50,000 |

|||||

|

2003 |

Mar.31 |

Balance c/d |

7,50,000 |

||||

|

Mar.01 |

Bank (ii) |

3,00,000 |

|||||

|

7,50,000 |

7,50,000 |

||||||

|

2003 |

2004 |

||||||

|

Apr.01 |

Balance b/d |

||||||

|

(i) 4,50,000, (ii) 3,00,000 |

7,50,000 |

Mar.31 |

Balance c/d |

7,50,000 |

|||

|

7,50,000 |

7,50,000 |

||||||

|

2004 |

2004 |

||||||

|

Apr.01 |

Balance b/d |

7,50,000 |

July 01 |

Furniture Disposal |

4,50,000 |

||

|

(i) 4,50,000, (ii) 3,50,000 |

2005 |

||||||

|

Mar.31 |

Balance c/d |

3,00,000 |

|||||

|

7,50,000 |

7,50,000 |

||||||

|

Accumulated Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2003 |

2003 |

||||||

|

Mar.31 |

Balance c/d |

37,500 |

Mar.31 |

Depreciation |

|||

|

(i) 33,750, (ii) 3,750 |

37,500 |

||||||

|

37,500 |

37,500 |

||||||

|

2004 |

2003 |

||||||

|

Mar.31 |

Balance c/d |

1,44,376 |

Apr.01 |

Balance b/d |

37,500 |

||

|

2004 |

|||||||

|

Mar.31 |

Depreciation |

||||||

|

(i) 62,438, (ii) 44,378 |

1,06,876 |

||||||

|

1,44,376 |

1,44,376 |

||||||

|

2004 |

2004 |

||||||

|

July.01 |

Furniture Disposal |

1,09,456 |

Apr.01 |

Balance b/d |

1,44,376 |

||

|

2005 |

July.01 |

Depreciation (i) |

13,268 |

||||

|

Mar.31 |

Balance c/d |

85,960 |

2005 |

||||

|

Mar.31 |

Depreciation (ii) |

37,772 |

|||||

|

1,95,416 |

1,95,416 |

||||||

|

Furniture Disposal Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2004 |

2004 |

||||||

|

Jul.01 |

Furniture |

4,50,000 |

Jul.01 |

Accumulated Dep. |

1,09,456 |

||

|

Jul.01 |

Bank |

2,25,000 |

|||||

|

Jul.01 |

Profit and Loss (Loss) |

1,15,544 |

|||||

|

4,50,000 |

4,50,000 |

||||||

Working Note:

Furniture (i)

|

Years |

Opening Balance |

Depreciation |

Closing Balance |

|||

|

2002 – 2003 |

4,50,000 |

– |

33,750 |

= |

4,16,250 |

|

|

2003 – 2004 |

4,16,250 |

– |

62,438 |

= |

3,53,812 |

|

|

2004 |

3,53,812 |

– |

13,268 |

(3 months) |

= |

3,40,544 |

|

1,09,456 |

||||||

|

Balance on July 01, 2004 |

3,40,544 |

|||||

|

Less: Sale on July 01, 2004 |

(2,25,000) |

|||||

|

Loss on sale of furniture |

1,15,544 |

|||||

Q7 : M/s Lokesh Fabrics purchased a Textile Machine on April 01, 2001 for Rs 1,00,000. On July 01, 2002 another machine costing Rs 2,50,000 was purchased . The machine purchased on April 01, 2001 was sold for Rs 25,000 on October 01, 2005. The company charges depreciation @15% p.a. on straight line method. Prepare machinery account and machinery disposal account for the year ended March 31, 2006.

Notes

There is a misprint in the question in the dates. The year 2001 has been mistakenly written as 2010.

The machinery was sold on October 01, 2005. In the book, it has been misprinted as October 01, 2010.

The books of accounts are to be prepared for the year ended March 31, 2006 and not March 31, 2011.

Answer :

|

Books of M/s. Lokesh Fabrics |

|||||||

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2002 |

||||||

|

Apr.01 |

Bank (i) |

1,00,000 |

Mar.31 |

Depreciation |

15,000 |

||

|

Mar.31 |

Balance c/d |

85,000 |

|||||

|

1,00,000 |

1,00,000 |

||||||

|

2002 |

2003 |

||||||

|

Apr.01 |

Balance b/d |

85,000 |

Mar.31 |

Depreciation |

|||

|

July.01 |

Bank (ii) |

2,50,000 |

(i) 15,000 + 28,125 |

43,125 |

|||

|

Mar.31 |

Balance c/d |

||||||

|

(i) 70,000, (ii) 2,21,875 |

2,91,875 |

||||||

|

3,35,000 |

3,35,000 |

||||||

|

2003 |

2004 |

||||||

|

Apr.01 |

Balance b/d |

Mar.31 |

Depreciation |

||||

|

(i) 70,000, (ii) 2,21,875 |

2,91,875 |

(i) 15,000, (ii) 37,500 |

52,500 |

||||

|

Mar.31 |

Balance c/d |

||||||

|

(i) 55,000, (ii) 1,84,375 |

2,39,375 |

||||||

|

2,91,875 |

2,91,875 |

||||||

|

2004 |

2005 |

||||||

|

Apr.01 |

Balance b/d |

Mar.31 |

Depreciation |

||||

|

(i) 5,500, (ii) 1,84,375 |

2,39,375 |

(i) 15,000, (ii) 37,500 |

52,500 |

||||

|

Mar.31 |

Balance c/d |

||||||

|

(i) 40,000, (ii) 1,46,875 |

1,86,875 |

||||||

|

2,39,375 |

2,39,375 |

||||||

|

2005 |

2005 |

||||||

|

Apr.01 |

Balance b/d |

Oct.01 |

Depreciation |

7,500 |

|||

|

(i) 40,000, (ii) 1,46,875 |

1,86,875 |

Oct.01 |

Machinery Disposal |

32,500 |

|||

|

2006 |

|||||||

|

Mar.31 |

Depreciation (ii) |

37,500 |

|||||

|

Mar.31 |

Balance c/d |

1,09,375 |

|||||

|

1,86,875 |

1,86,875 |

||||||

|

Machinery Disposal Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2005 |

2005 |

||||||

|

Oct.01 |

Machinery |

32,500 |

Oct.01 |

Bank |

25,000 |

||

|

Oct.01 |

Profit and Loss |

7,500 |

|||||

|

32,500 |

32,500 |

||||||

Q8 : The following balances appear in the books of Crystal Ltd, on Jan 01, 2005

Rs Machinery account on 15,00,000

Provision for depreciation account 5,50,000

On April 01, 2005 a machinery which was purchased on January 01, 2002 for Rs 2,00,000 was sold for Rs 75,000. A new machine was purchased on July 01, 2005 for Rs 6,00,000. Depreciation is provided on machinery at 20% p.a. on Straight line method and books are closed on December 31 every year. Prepare the machinery account and provision for depreciation account for the year ending December 31, 2005.

Note*: There is a misprint in the question. The year 2005 has been mistakenly written as 2010. Accordingly, we have worked out the solution for the year 2005.

Answer:

|

Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2005 |

2005 |

||||||

|

Jan.01 |

Balance b/d |

15,00,000 |

Apr.01 |

Machinery Disposal |

2,00,000 |

||

|

(13,00,000 + 2,00,000) |

|||||||

|

Jul.01 |

Bank |

6,00,000 |

Dec.31 |

Balance c/d |

19,00,000 |

||

|

21,00,000 |

21,00,000 |

||||||

|

Provision for Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2005 |

2005 |

||||||

|

Apr.01 |

Machinery Disposal |

1,30,000 |

Jan.01 |

Balance b/d |

5,50,000 |

||

|

Apr.01 |

Balance c/d |

7,50,000 |

Apr.01 |

Depreciation |

10,000 |

||

|

Dec.31 |

Depreciation |

||||||

|

(i) 2,60,000, (ii) 60,000 |

3,20,000 |

||||||

|

8,80,000 |

8,80,000 |

||||||

Working Note:

Machine Sold on July 01, 2005

|

(i) |

Years |

Opening Balance |

Depreciation |

Closing Balance |

|||||

|

2002 |

2,00,000 |

– |

40,000 |

= |

1,60,000 |

||||

|

2003 |

1,60,000 |

– |

40,000 |

= |

1,20,000 |

||||

|

2004 |

1,20,000 |

– |

40,000 |

= |

80,000 |

||||

|

2005 |

80,000 |

– |

10,000 |

= |

70,000 |

||||

|

Accumulated Depreciation |

= |

1,30,000 |

|||||||

|

Value on April 01, 2005 |

= |

(70,000) |

|||||||

|

Less: Sale |

= |

75,000 |

|||||||

|

Profit on sale of Machinery |

5,000 |

||||||||

|

Machinery Disposal Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2005 |

2005 |

||||||

|

Apr.01 |

Machinery |

2,00,000 |

Apr.01 |

Provision for Depreciation |

1,30,000 |

||

|

Apr.01 |

Profit and Loss (Profit) |

5,000 |

Apr.01 |

Bank |

75,000 |

||

|

2,05,000 |

2,05,000 |

||||||

Q9 :M/s. Excel Computers has a debit balance of Rs 50,000 (original cost Rs 1,20,000) in computers account on April 01, 2000. On July 01, 2000 it purchased another computer costing Rs 2,50,000. One more computer was purchased on January 01, 2001 for Rs 30,000. On April 01, 2004 the computer which has purchased on July 01, 2000 became obsolete and was sold for Rs 20,000. A new version of the IBM computer was purchased on August 01, 2004 for Rs 80,000. Show Computers account in the books of Excel Computers for the years ended on March 31, 2001, 2002, 2003, 2004 and 2005. The computer is depreciated @10 p.a. on straight line method basis.

Note*: There is a misprint in the question. The year 2001 has been mistakenly written as 2010. Accordingly, we have worked out the solution for the years ending March 31, 2001 to March 31, 2005.

Answer :

|

Books of M/s Excel Computers |

|||||||

|

Computer Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2000 |

2001 |

||||||

|

Apr.01 |

Balance b/d (i) |

50,000 |

Mar.31 |

Depreciation |

|||

|

Jul.01 |

Bank (ii) |

2,50,000 |

(i) 12,000, (ii) 18,750, |

||||

|

2001 |

(iii) 750 |

31,500 |

|||||

|

Jan.01 |

Bank (iii) |

30,000 |

Mar.31 |

Balance c/d |

|||

|

(i) 38,000, (ii) 2,31,250, |

|||||||

|

(iii) 29,250 |

2,98,500 |

||||||

|

3,30,000 |

3,30,000 |

||||||

|

2001 |

2002 |

||||||

|

Apr.01 |

Balance b/d |

Mar.31 |

Depreciation |

||||

|

(i) 38,000, (ii) 2,31,250, |

(i) 12,000 (ii) 25,000, |

||||||

|

(iii) 29,250 |

2,98,500 |

(iii) 3,000 |

40,000 |

||||

|

Mar.31 |

Balance c/d |

||||||

|

(i) 26,000 (ii) 2,06,250, |

|||||||

|

(iii) 26,250 |

2,58,500 |

||||||

|

2,98,500 |

2,98,500 |

||||||

|

2002 |

2003 |

||||||

|

Apr.01 |

Balance b/d |

Mar.31 |

Depreciation |

||||

|

(i) 26,000 (ii) 2,06,250, |

(i) 12,000, (ii) 25,000, |

40,000 |

|||||

|

(iii) 26,250 |

2,58,500 |

Mar.31 |

(iii) 3,000 |

||||

|

Balance c/d |

|||||||

|

(i) 14,000, (ii) 1,81,250, |

|||||||

|

(iii) 23,250 |

2,18,500 |

||||||

|

2,58,500 |

2,58,500 |

||||||

|

2003 |

2004 |

||||||

|

Apr.01 |

Balance b/d |

Mar.31 |

Depreciation |

||||

|

(i) 14,000, (ii) 1,81,250, |

(i) 12,000, (ii) 25,000, |

40,000 |

|||||

|

(iii) 23,250 |

2,18,500 |

(iii) 3,000 |

|||||

|

Mar.31 |

Balance c/d |

||||||

|

(i) 2,000, (ii) 1,56,250, |

|||||||

|

(iii) 20,250 |

1,78,500 |

||||||

|

2,18,500 |

2,18,500 |

||||||

|

2004 |

2004 |

||||||

|

Apr.01 |

Balance c/d |

Apr.01 |

Bank (ii) |

20,000 |

|||

|

(i) 2,000, (ii) 1,56,250, |

Apr.01 |

Profit and Loss (Loss) |

1,36,250 |

||||

|

(iii) 20,250 |

1,78,500 |

2005 |

|||||

|

Aug.01 |

Bank (iv) |

80,000 |

Mar.31 |

Depreciation |

10,333 |

||

|

(i) 2,000, (iii) 3,000, (iv) 5,333 |

|||||||

|

Mar.31 |

Balance c/d |

||||||

|

(iii) 17,250, (iv) 74,667 |

91,917 |

||||||

|

2,58,500 |

2,58,500 |

||||||

Note: As per the solution, the closing balance, as on 31st March, 2005 is Rs 91,917; however, as per the book it is Rs 80,583.

Q10 :Carriage Transport Company purchased 5 trucks at the cost of Rs 2,00,000 each on April 01, 2001. The company writes off depreciation @ 20% p.a. on original cost and closes its books on December 31, every year. On October 01, 2003, one of the trucks is involved in an accident and is completely destroyed. Insurance company has agreed to pay Rs 70,000 in full settlement of the claim. On the same date the company purchased a second hand truck for Rs 1,00,000 and spent Rs 20,000 on its overhauling. Prepare truck account and provision for depreciation account for the three years ended on December 31, 2003. Also give truck account if truck disposal account is prepared.

Note*: There is a misprint in the question. The date of purchase of 5 trucks should be April 01, 2001. It has been mistakenly written as April 01, 2010.

Answer:

|

Books of Carriage Transport Company |

|||||||

|

Truck Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Apr.01 |

Bank |

10,00,000 |

Dec.31 |

Balance c/d |

10,00,000 |

||

|

10,00,000 |

10,00,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d |

10,00,000 |

Dec.31 |

Balance c/d |

10,00,000 |

||

|

10,00,000 |

10,00,000 |

||||||

|

2003 |

2003 |

||||||

|

Jan.01 |

Balance b/d |

10,00,000 |

Oct.01 |

Truck Disposal |

2,00,000 |

||

|

Oct.01 |

Bank |

1,20,000 |

Dec.31 |

Balance c/d |

9,20,000 |

||

|

11,20,000 |

11,20,000 |

||||||

|

Provision for Depreciation Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Dec.31 |

Balance c/d |

1,50,000 |

Dec.31 |

Depreciation |

1,50,000 |

||

|

1,50,000 |

1,50,000 |

||||||

|

2002 |

2002 |

||||||

|

Dec.31 |

Balance c/d |

3,50,000 |

Jan.01 |

Balance c/d |

1,50,000 |

||

|

Dec.31 |

Depreciation |

2,00,000 |

|||||

|

3,50,000 |

3,50,000 |

||||||

|

2003 |

2003 |

||||||

|

Oct.01 |

Truck Disposal |

1,00,000 |

Jan.01 |

Balance b/d |

3,50,000 |

||

|

Oct.01 |

Balance c/d |

4,46,000 |

Oct.01 |

Depreciation (9 Months) |

30,000 |

||

|

Dec.31 |

Depreciation |

||||||

|

(1,60,000 + 6,000) |

1,66,000 |

||||||

|

5,46,000 |

5,46,000 |

||||||

|

Truck Disposal Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2003 |

2003 |

||||||

|

Oct.01 |

Truck |

2,00,000 |

Oct.01 |

Provision for Depreciation |

1,00,000 |

||

|

Oct.01 |

Insurance Co. (Insurance Claim) |

70,000 |

|||||

|

Oct.01 |

Profit and Loss (Loss) |

30,000 |

|||||

|

2,00,000 |

2,00,000 |

||||||

Working Note

Truck involved in accident

|

Opening Balance |

Depreciation |

Closing Balance |

|||||||

|

Apr.01, 2001 |

2,00,000 |

– |

30,000 |

= |

1,70,000 |

||||

|

Jan.01, 2002 |

1,70,000 |

– |

40,000 |

= |

1,30,000 |

||||

|

Jan.01, 2003 |

1,30,000 |

– |

30,000 |

= |

1,00,000 |

||||

|

Accumulated Depreciation |

= |

1,00,000 |

|||||||

|

Value on Oct.01, 2003 |

= |

1,00,000 |

|||||||

|

Less: Insurance Claim |

= |

70,000 |

|||||||

|

Loss on Accident |

30,000 |

||||||||

Q11 :Saraswati Ltd. purchased a machinery costing Rs 10,00,000 on January 01, 2001. A new machinery was purchased on 01 May, 2002 for Rs 15,00,000 and another on July 01, 2004 for Rs 12,00,000. A part of the machinery which originally cost Rs 2,00,000 in 2001 was sold for Rs 75,000 on October 31, 2004. Show the machinery account, provision for depreciation account and machinery disposal account from 2001 to 2005 if depreciation is provided at 10% p.a. on original cost and account are closed on December 31, every year.

Answer :

|

Books of Saraswati Ltd. Machinery Account |

|||||||

|

Dr. |

Cr. |

||||||

|

Date |

Particulars |

J.F. |

Amount Rs |

Date |

Particulars |

J.F. |

Amount Rs |

|

2001 |

2001 |

||||||

|

Jan.01 |

Bank (i) |

10,00,000 |

|||||

|

(8,00,000 + 2,00,000) |

Dec.31 |

Balance c/d |

10,00,000 |

||||

|

10,00,000 |

10,00,000 |

||||||

|

2002 |

2002 |

||||||

|

Jan.01 |

Balance b/d |

10,00,000 |

Dec.31 |